Bridging the Lifecycle Gap: Managing Semiconductor Obsolescence in Automotive ECUs

Real-world case insights from Tier-1 automotive suppliers, illustrating measurable improvements in supply chain resilience, cost control, and sustainability.

Add bookmark

The modern automobile is no longer just a mechanical marvel, it is a distributed computing platform on wheels. Today’s vehicles contain upward of 80 to 150 electronic control units (ECUs), each embedded with hundreds of semiconductor devices. These chips manage everything from braking and steering to infotainment, driver assistance, and battery management. As the industry accelerates toward electrification and autonomous driving, that semiconductor content is expected to double over the next decade.

Yet, there is a growing disconnect between how long a vehicle is designed to last and how long the chips that power it remain available. Automakers engineer vehicles for service lives of 15 years or more, but many semiconductors reach End-of-Life (EOL) status in less than seven. The pace of change in semiconductor technology driven by innovation, new process nodes, and market shifts means that devices can become obsolete long before a vehicle even finishes production.

This lifecycle mismatch has turned semiconductor obsolescence into one of the most underestimated but critical risks facing the automotive industry. When a key component is discontinued, ECU manufacturers must choose between making a large last-time buy, requalifying an alternative part, or redesigning entire modules all of which can introduce cost, delay, and risk.

The 2021 global chip shortage exposed how vulnerable automotive supply chains had become. Production lines were halted, billions were lost in revenue, and OEMs learned that semiconductors are not just components they are strategic assets. For instance, Nexperia experienced widespread supply disruptions that aƯected multiple automotive Tier-1s, highlighting how a single supplier’s constraints ripple across the value chain. Similarly, ON Semiconductor’s temporary shortage impacted production schedules for various OEMs, reinforcing that obsolescence is a recurring, structural issue that must be addressed through proactive lifecycle management.

Understanding the Challenge

A single automotive ECU can contain more than 300 unique electronic components like microcontrollers, power devices, sensors, and passives each sourced from multiple suppliers across the globe. Every component has its own product roadmap, lifecycle, and discontinuation timeline. While some standard resistors and capacitors stay in production for decades, more complex integrated circuits may be replaced every three to five years as technology evolves.

This creates a persistent risk of supply chain misalignment. The situation is compounded by the stringent validation and safety certification requirements in automotive electronics. A simple part change often triggers new qualification testing, software adjustments, or safety documentation updates, all of which require engineering time and cost.

Traditional responses to obsolescence like reacting to EOL notices with urgent redesigns or stockpiling last-time buys are expensive and ineƯicient. Excess inventory ties up working capital and risks future scrap if demand forecasts are inaccurate. On the other hand, late redesigns can delay vehicle launches or compromise functional safety re-certification under ISO 26262.

The fundamental challenge is therefore not just sourcing replacement parts, but synchronizing component lifecycles with the vehicle lifecycle itself. Without structured foresight, obsolescence becomes a ticking clock embedded in every control unit that leaves the production line.

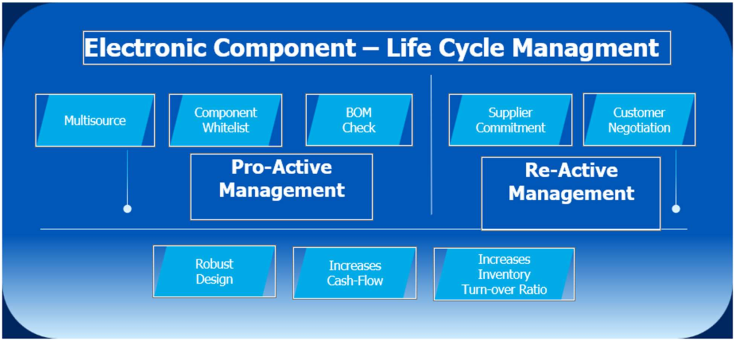

From Reactive to Proactive: A Smarter Strategy

Forward-looking Tier-1 suppliers are moving away from firefighting EOL issues and embracing predictive lifecycle management. This proactive approach begins with enriching the company’s internal electronic component database. Instead of storing only basic data such as part numbers, footprints, and suppliers, the new paradigm includes detailed lifecycle attributes estimated years to EOL, technology maturity, sourcing risk, and available alternatives.

Source: AI-generated image

By linking this enriched database to supplier portals, lifecycle forecasting tools, and automated alerts, organizations can identify high-risk components as early as the design phase. Engineers can then avoid technologies with short roadmaps, pre-qualify alternatives, or choose suppliers with robust longevity programs.

The impact of such foresight is measurable. At one Tier-1 supplier, implementing a multisourcing strategy across passive components led to dramatic results within two years:

- Inventory turnover improved by 57%,

- EOL-driven redesigns dropped by 82%, and

- The share of BOM parts with approved multi-source options grew from 10% to 74%.

These gains demonstrate that lifecycle intelligence is not just a compliance measure it is a profit and stability enabler. By embedding lifecycle awareness into design workflows, companies transform their culture from reactive problem-solving to strategic risk mitigation.

Mitigating the Unavoidable: When EOL Hits

Even with robust forecasting, obsolescence cannot be eliminated entirely. When a semiconductor supplier announces an EOL, manufacturers face several choices:

1. Secure a Last-Time Buy (LTB) to cover future production and service demand.

2. Redesign the aƯected ECU to accommodate a new or equivalent component.

3. Negotiate a continuation supply through an authorized aftermarket manufacturer.

Each option carries financial implications. Over-ordering in an LTB can result in excess inventory that becomes scrap if demand drops. Under-ordering risks production interruptions and service shortages. The solution lies in accurate, data-driven forecasting integrating historical demand, vehicle production schedules, and aftermarket service requirements.

Some suppliers have developed advanced analytics dashboards that combine these inputs to predict optimal LTB quantities. Others employ machine-learning models that identify potential EOL risks months before oƯicial notices are released. These predictive tools allow manufacturers to make informed, timely decisions and reduce financial exposure when obsolescence is inevitable.

Sharing the Risk: Collaboration Across the Value Chain

Obsolescence management is not the responsibility of a single player; it is a shared challenge across the entire value chain from chipmakers to Tier-1s to OEMs. The most resilient companies are those that have shifted from risk-bearing to risk-sharing models.

With customers, proactive communication is key. Dashboards that show component lifecycle status in real time help OEMs understand risk exposure and plan service strategies. Some suppliers have even implemented advance-payment or pre-buy agreements with customers to finance long-term inventory for critical parts, improving transparency and trust.

With semiconductor suppliers, collaboration can take the form of long-term service agreements (LTSAs) that guarantee supply for legacy nodes, or buyback and consignment programs that ensure no party bears the entire cost of over-ordering.

There are successful examples in the industry: ON Semiconductor’s partnerships with Zeekr and Magna, for instance, demonstrate how long-term collaboration can stabilize both financial and operational planning. Similarly, during the Nexperia automotive chip shortage, proactive collaboration between Tier-1s and OEMs helped maintain continuity in highdemand production. Such arrangements transform the traditional buyer-supplier dynamic into a cooperative resilience model

A Path Toward Sustainable Electronics

Semiconductor lifecycle management has evolved from a niche procurement activity into a strategic discipline central to automotive reliability, safety, and sustainability. Every avoided redesign reduces engineering waste, lowers validation energy, and extends the usable life of electronics contributing directly to environmental goals.

Sustainability in electronics is no longer limited to recycling or reducing carbon footprint; it includes designing products that can remain in service longer, with components that are supportable throughout their operational lifespan.

By combining proactive data enrichment, multi-sourcing, and collaborative risk-sharing, ECU manufacturers can reduce the frequency of redesigns, stabilize margins, and extend the lifecycle of vehicles well beyond the availability window of individual chips.

The next frontier lies in AI-driven predictive analytics. Machine-learning models can forecast obsolescence trends years in advance by analyzing supplier announcements, wafer-fab transitions, and market signals. Integrating these predictions directly into design and sourcing systems could redefine how the automotive industry manages electronic reliability for the next generation of smart, connected vehicles.